Comparative Valuation of Employee Stock Options Using CRR and Enhanced American Models with Vesting and Exit Effects

Article Sidebar

-

Employee Stock Options, Enhanced American Model, Cox-Ross-Rubinstein Model, Vesting Period, Exit Risk, Fair Value Measurement

Abstract

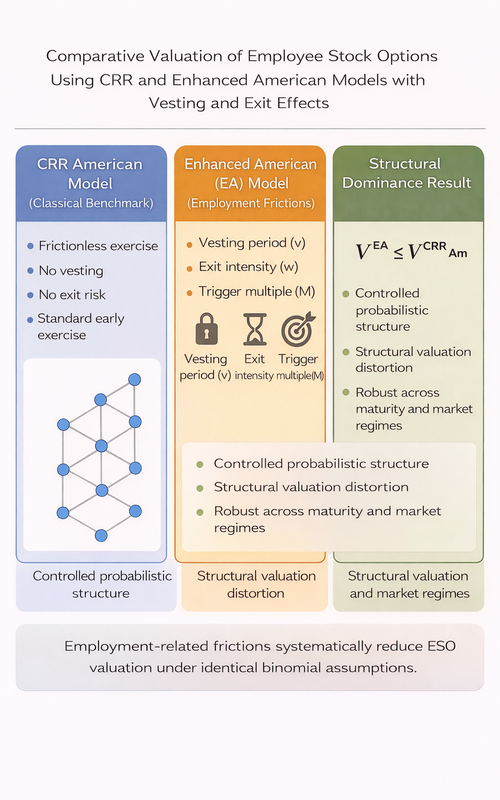

Employee stock options (ESOs) are required to be measured at grant-date fair value under existing accounting standards, yet classical lattice models typically assume frictionless exercise behavior. In practice, ESO contracts incorporate vesting restrictions, employee exit risk, and behavioral exercise triggers that can materially affect valuation outcomes. This study provides a structural comparison between the Cox-Ross-Rubinstein (CRR) American model and the Enhanced American (EA) framework within a unified binomial setting in which the probabilistic return process constant to isolate employment-related frictions. An analytical dominance result is established, showing that EA valuations remain strictly below the CRR American benchmark under these frictions. Numerical experiments confirm the theoretical ordering and quantify its economic magnitude: under moderate frictions, valuation gaps remain limited to approximately 2-3%, whereas under high exit intensity and conservative trigger thresholds, the discount expands substantially to approximately 65-69%, particularly for long-dated and near-the-money contracts. Heatmap analysis across volatility and dividend regimes further demonstrates that this dominance ordering persists under economically relevant parameter variations. The findings indicate that employment-related frictions constitute a materially significant component of ESO valuation and that model choice within fair-value measurement frameworks can meaningfully influence reported compensation expenses.

References

Abdurakhman, Subanar, S. Guritno, and Z. Soejoeti (2006). Valuing Trinomial Option Pricing with Pseudoinverse Matrix. Journal of the Indonesian Mathematical Society, 12(2); 131–140

Adrianto, A., A. Ben-Ner, J. Sockin, and A. Urtasun (2024). Sharing Is Caring: Employee Stock Ownership Plans and Employee Well-Being in U.S. Manufacturing. Technical Report 17233

Alifianty, S. and A. I. Susanty (2016). Influence of Employee Stock Option Program and Job Satisfaction on Employee Commitment (A Case Study of a Telephone Company in Indonesia). Pertanika Journal of Social Sciences and Humanities, 24; 215–226

Ammann, M. and R. Seiz (2004). Does the Model Matter? A Valuation Analysis of Employee Stock Options. Journal of Banking and Finance, 22(12); 3009–3034

Aran, Y. (2018). Beyond Covenants Not to Compete: Equilibrium in High-Tech Startup Labor Markets. Stanford Law Review, 70; 1235–1294

Arora, M. K. and S. Kaur (2024). Exercise Decision of Employee Stock Options: Does Herding Bias Influence the Employees’ Decision? Managerial Finance, 50(4); 653–675

Athar, M. (2020). Employee Stock Option Plans: A Meta-Analysis (Understanding Impact of ESOPs through Literature). Studies in Business and Economics, 15(15); 100–114

Bahaji, H. (2018). Are Employee Stock Option Exercise Decisions Better Explained through Prospect Theory? Annals of Operations Research, 262(2); 335–359

Boyle, P. P. (1986). Option Valuation Using a Three-Jump Process. Journal of Financial Economics, 17; 71–83

Boyle, P. P. (1988). A Lattice Framework for Option Pricing with Two State Variables. Journal of Financial and Quantitative Analysis, 23(1); 1–12

Cable, A. J. B. (2025). Stock Options of Adhesion. Journal of Corporate Law, 50; 1–35

Chendra, E., K. A. Sidarto, A. Sukmana, and L. Chin (2022). Pricing Employee Stock Options with an Asian Style Using a Modified Binomial Method: Case Study from Indonesian ESO. International Journal of Applied Mathematics, 35(2); 233–247

Cox, J. C., S. A. Ross, and M. Rubinstein (1979). Option Pricing: A Simplified Approach. Journal of Financial Economics, 7(3); 229–263

Devianto, D., R. D. Safitri, J. Herli, and Maiyastri (2018). On the Infinitely Divisible of Meixner Distribution. Science and Technology Indonesia, 3(4); 147–150

Financial Accounting Standards Board (2021). Accounting Standards Codification (ASC) Topic 718: Compensation—Stock Compensation

Hull, J. and A. White (1987). The Pricing of Options on Assets with Stochastic Volatilities. Journal of Finance, 42(2); 281–300

Hull, J. C. (2022). Options, Futures, and Other Derivatives. Pearson Education, New York, 11 edition

Ikatan Akuntan Indonesia (2014). Pernyataan Standar Akuntansi Keuangan 53: Pembayaran Berbasis Saham (Revisi 2014). (in Indonesian)

International Accounting Standards Board (2016). IFRS 2: Share-Based Payment

Lesmana, D. C., R. T. A. Ramadhan, S. Nurjanah, and V. S. Dharmawan (2025). Pricing Employee Stock Option Using Trinomial Tree Method. Barekeng: Journal of Mathematics and Its Applications, 19(2); 709–720

Leung, T. (2022). Employee Stock Options: Exercise Timing, Hedging, and Valuation. World Scientific Publishing Co., Singapore

Pendleton, A. and A. Robinson (2023). Employee Behavior in Employee Stock Option Plans: Why Do Some Employees Acquire Company Stock? Human Resource Management, 61(6); 643–659

PT Telkom Indonesia (Persero) Tbk. (2022). Annual Report 2022

Sayed, A. and S. S. R. Muhammad (2022). A Simulation Study on the Simulated Annealing Algorithm in Estimating the Parameters of Generalized Gamma Distribution. Science and Technology Indonesia, 7(1); 84–90

Tian, Y. S. A. M. (1998). A Trinomial Option Pricing Model Dependent on Skewness and Kurtosis. International Review of Economics and Finance, 7(3); 315–330

Wang, B., H. Wang, M. Wang, and X. T. Zhang (2025). Unionization and Rank-and-File Employee Stock Options: Empirical Evidence. Managerial Finance, 51(12); 1817–1830

Yusof, N. M., I. Q. Alias, A. J. Md Kassim, and F. L. N. Mohd Zaidi (2021). Determining the Credit Score and Credit Rating of Firms Using the Combination of KMV-Merton Model and Financial Ratios. Science and Technology Indonesia, 6(3); 105–112

Authors

This work is licensed under a Creative Commons Attribution 4.0 International License.